Newsletter

Building Digital Pharma Supply Chain

India's Pharma Supply Chain: Does the Industry Have What It Takes to Win?

Leading firms can help the country become a global hub for low-cost manufacturing and R&D, but the journey will require new ways of working and a supply chain transformation.

Capturing Growth in a Complex Landscape

The past decade has been a time of growth for the Indian pharmaceutical industry. From 2005 to 2015, the revenue of the top 10 pharma companies grew at about 19 percent while the industry grew at about 18 percent. India’s generic market continues to expand; after growing by 22 percent in the past decade, Indian exports now have a 20 percent share of global exports by volume. By 2020, India is expected to capture 6 percent to 7 percent of a $760 billion global generics market. The Indian pharma market now stands at $30 billion, with the highest number of sites approved by the US Food and Drug Administration (FDA) after the United States itself—a clear indicator of the pivotal role Indian companies play in both local and global markets and the growing appetite to invest in the country.

As a global pharma player, India is going through an interesting phase. Companies have fearlessly embarked on a growth trajectory aspiring to become a hub for low-cost manufacturing and R&D, and yet they are also facing a unique set of local and global challenges that are creating significant pressure to tighten the end-to-end operations. The landscape has become more complex with an interplay of factors that make it a challenging space, even for the well-established players. In addition, observers expect the goods and services tax (GST) regime to influence the sourcing, manufacturing, and distribution footprint, with particular impact on transportation and warehousing.1 Companies are looking at the next phase of growth, but there is a significant gap between the strategic vision and operational reality. Products have proliferated exponentially and become more complex, driven by patients’ growing therapeutic needs. Fragmentation at every stage of the value chain is a direct hit on supply chain efficiency. Quality issues and price pressures have spiraled across the value chain, triggered by more regulatory scrutiny. Infrastructure, although better than in the past, is still a concern. Despite these challenges, pharma companies are expected to drive topline and bottom-line growth while also improving shareholder value. Pharma supply chains in India now face greater pressure to enhance their performance to prepare for the future and create a competitive advantage.

To assess the state of India’s end-to-end pharma supply chain, which serves local and global markets, and to identify the imperatives for the future, we conducted a study in collaboration with the Organisation of Pharmaceutical Producers of India (OPPI) and the Indian Pharmaceutical Association (IPA). As part of this study, we interviewed CEOs and supply chain executives in medium and large Indian pharma companies. Our study addresses three questions:

- What is the current state of India’s pharma supply chain?

- What are the supply chain challenges?

- How can companies use the supply chain to gain a competitive advantage?

The Current State of the Supply Chain

With a pivotal position in the global network, India’s pharmaceutical industry is poised to exceed $55 billion by 2020, according to estimates by the Associated Chambers of Commerce of India (ASSOCHAM). Facing competition from domestic and multinational players, Indian pharma companies have started to diversify and are taking bold steps to strengthen their portfolio. A few initiatives include developing capabilities to manufacture more differentiated and complex generics, investing in innovators, and building capacity to manufacture biosimilars.

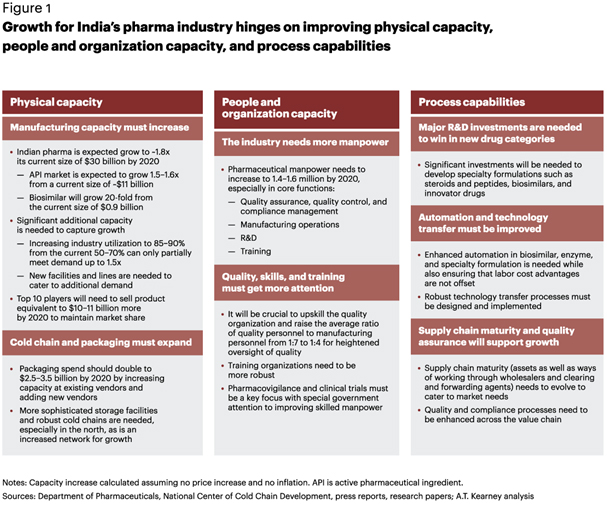

Although the growth vision looks bright, there is much headway to be made across multiple fronts. Our assessment indicates that forward-thinking firms are turning their attention to building both their capacity and their capabilities (see figure 1). There is much headway to be made across each of these areas.

A key challenge Indian organizations face is that the business differentiator is shifting from being reverse-engineering experts to having improved operational performance parameters such as service level and cost to deliver. Competition is fierce. Pressure to bring down the cost of drugs is an additional element—resulting in the need to reexamine the supply chain. Most Indian companies have successfully figured out how to reverse engineer and manufacture generic drugs but have paid little or no attention to operational aspects.

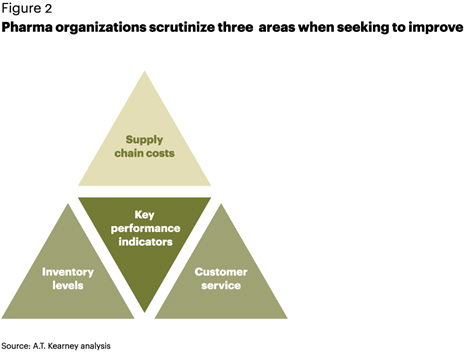

To assess the state of the industry, we identified three key performance indicators that organizations rely on to gauge their overall supply chain health and readiness for growth (see figure 2).

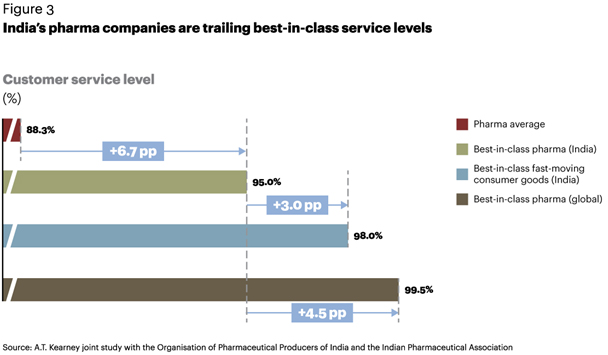

Customer service. Big or small, pharmaceutical companies strive to ensure their products are available across the entire supply chain. Maintaining product quality also ensures good service levels. Best-in-class pharma companies in India operate at a 95 percent service level, which is 3 percentage points lower than the best-in-class Indian fast-moving consumer goods (FMCG) companies and 4.5 points lower than best-in-class global pharma companies (see figure 3). While it would be challenging for India’s pharma companies to meet these service levels in the near term, the industry average is almost 7 points lower than best in class, indicating potential headroom for integrating the supply chain over the medium to long term.

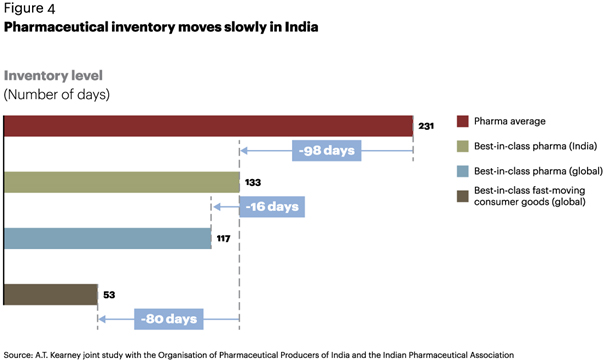

Inventory levels. Fragmentation has resulted in a large number of stocking locations. India has a multitiered distribution network through clearing and forwarding agents and stockists. Because of long manufacturing lead times and regulatory requirements, pharma companies usually maintain higher stock levels than other industries, even at the cost of writing off expired inventory. Looking at the pharma industry as a whole, the average inventory level is 98 days higher than India’s best in class—a huge difference (see figure 4). A comparison of best-in-class pharma in India against best-in-class FMCG firms globally points to an additional difference of 80 days of inventory, reinforcing the clear need for better planning and inventory management.

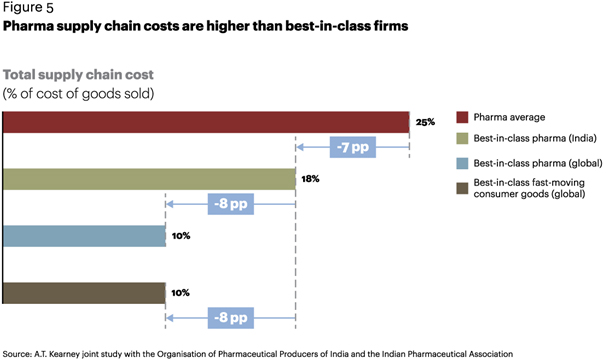

Supply chain costs. Supply chain costs depend heavily on the type of product. Specialized cold chain requirements for vaccines and other complex formulations can significantly increase supply chain cost. India’s best-in-class pharma is 8 percentage points higher than both the best-in-class global FMCG firms and best-in-class global pharma (see figure 5).

However, the industry average is 15 percentage points higher than the global best in class, which indicates suboptimal routes, high transportation costs, and issues with storage, specifically for high-risk and conditioned products. On average, manufacturing conversion costs account for nearly 75 percent of total supply chain cost, with distribution responsible for the remainder.

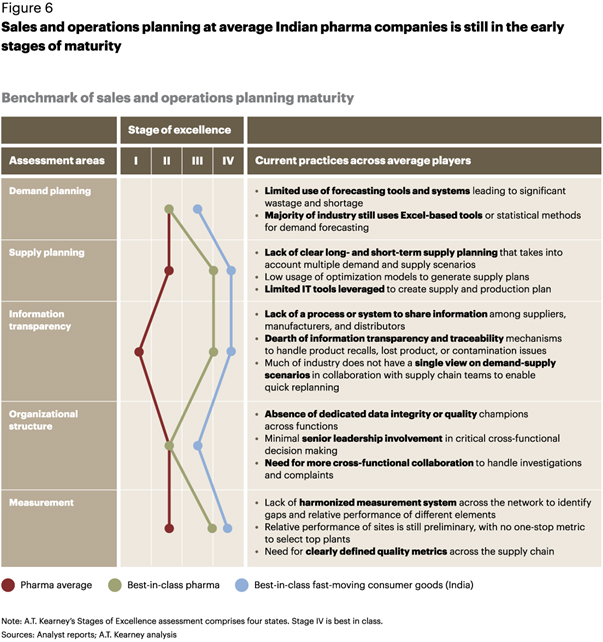

Our study shows that in each of the three parameters above, Indian pharma companies lag best-in-class standards. In addition we benchmarked sales and operations planning (S&OP) processes for the industry across five key dimensions (see figure 6).

Overall the industry is still in the early stages of maturity. Sustainable growth will require covering significant ground. An array of underlying factors are preventing companies from closing this supply chain performance gap.

Supply Chain Challenges

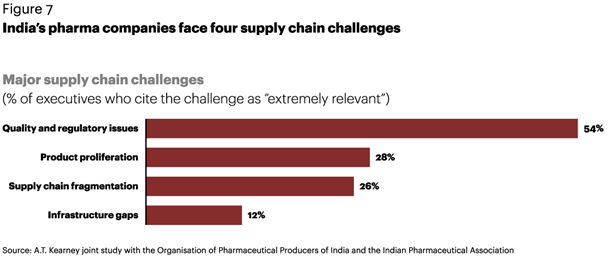

The executives we surveyed admit they are struggling with a number of challenges that are affecting the overall performance of their supply chains. Based on their responses, four issues emerge (see figure 7).

Quality and regulatory issues

Quality continues to be a hot topic in India’s pharmaceutical industry, with greater scrutiny coming from global regulatory agencies. With regard to exports, FDA issues have become more frequent and value-destroying. Large and small pharmaceutical companies alike have taken a hit in the headlines over the FDA’s concerns about quality. Plant shutdowns, import bans on specific products, and critical observations across the value chain have put a spotlight on exports, which is affecting companies’ revenue and credibility. In the domestic market, the Central Drugs Standard Control Organization (CDSCO) has increased the coverage and frequency of inspections to address the issue of low-quality drugs.

With 600 to 700 FDA-approved sites in India, global regulatory agencies are inspecting sites more often. In the past eight years, the FDA has identified more than 800 issues. In 2015 alone, 10 companies were issued warning letters—a 25 percent increase from 2014. Three of those companies were among India’s top 15 pharmaceutical firms. From 2014 to 2015, there was a 28 percent increase in Center for Drug Evaluation and Research FDA Form 483 observations, with 95 percent of the observations related to deficiencies in drug quality assurance.2 These observations point to a few of the FDA’s usual suspects, including lack of data integrity and falsification, low adherence to standard operating procedures, weak documentation practices, lack of data traceability, high cross-contamination, and poor validation of equipment and instruments.

Quality issues have deepened and widened over time and are not restricted to the production floor. In fact, more issues are occurring across the value chain:

Procurement. Issues with the quality of raw materials have spiraled over the past few years, leading to batch failures, production delays, and lack of availability of resources across the plant.

Manufacturing. Plant shutdowns and an inability to get certified by global regulatory agencies have created significant unused capacity across the network.

Logistics. Post-market issues such as complaints, rejects, and product failures are having a direct impact on storage, handling, and cost to discard rejected products.

R&D. Specifically for export products, lack of quality control in R&D has led to more failures of trial batches, causing delays in product launches.

Pricing regulation impact. Drugs (Price Control) Order (DPCO) 2013 stipulates that stock must be recalled for relabeling in the event of price changes, which results in significant wastage and loss of shelf life. In addition, pressure has increased as a result of the recent DPCO 2016, which adds 106 new drugs to the National List of Essential Medicines (NLEM) and removes 70 others.

Interestingly, of the respondents who indicated regulations and quality are relevant issues, 70 percent attribute the challenge to controllable internal issues such as lack of data checks for accuracy, poor product testing, and low qualification and validation of equipment. The remaining 30 percent point to external factors with sourcing and suppliers, such as an unknown particle in a raw material or a cold storage failure at the vendor site, and processes related to diverse regulatory requirements across countries.

Product proliferation

New product development, new dosage forms, enhanced formulations, and changes in packaging and labeling to cater to new markets are expanding the product portfolio. Leading Indian players launch anywhere from 15 to 30 products/SKUs a year. This has several implications for the supply chain, including higher manufacturing and distribution costs, more inventory, and a larger supplier base. Several underlying factors contribute to this:

Changing consumer demographics. Non-communicable diseases such as diabetes, cardiovascular disease, cancer, and chronic pain are on the rise in India and are rapidly moving toward early-age onset. This is attributed to lifestyle changes and poor diet, leading to a higher incidence of these diseases in rural, tier 3 segments of India. Studies indicate the peak occurrence could be a decade earlier than in Western countries. Top pharma players are including new molecules in their portfolios to cater to these emerging therapeutic segments. This could call for more plants, more manufacturing lines, and new technologies to support production, thereby adding significant complexity to the existing supply chain network.

Increased competition. Multiple products are on the market with very similar specifications, bioequivalence, and price points, marketed by both Indian and multinational firms. This fuels the need to continuously innovate and reduce the costs of existing drugs to remain competitive. Process enhancements are a large part of a pharma company’s pipeline. In fact, our study indicates 10 to 12 percent of capacity gets used in unsuccessful trial batches, affecting the production facility’s overall use and manufacturing flexibility.

Varying regulatory requirements across export markets. As companies expand into new markets, regulations vary across regions. Specification requirements and guidelines for labeling and packaging are governed by the pertinent health authorities. Product specifications need to be customized, and labels need to be printed according to guidelines, which increases the number of production runs for the same product, adds strain on labeling and packaging, and increases the number of stock-keeping units (SKUs). In India, the bigger issue is the sizable gap in regulatory standards for local approval compared with what is required for the largest export markets, including the United States and the United Kingdom.

Supply chain fragmentation

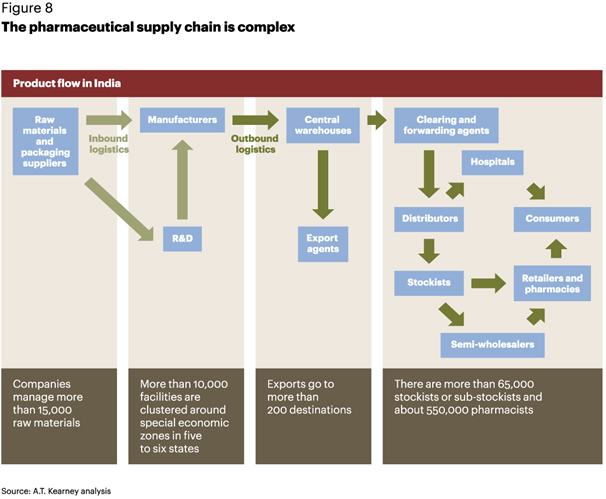

India’s pharmaceutical value chain is very complex and in some parts even poses concerns about product quality and safety, causing multiple repercussions. The sheer number of players at each stage and the lack of integration across the network have an impact on visibility and traceability of products as they move (see figure 8).

An array of elements cause complexity across the network:

Large number of vendors. In the next five years, a pharma company’s active supply base will double because of an increase in exports and growth of intermediates, excipients, and other raw materials. With companies exploring new synthesis routes and new technologies, raw material requirements are far more complex, and their availability is scattered. Multiple vendors with varying requirements, lack of clear categorization, lack of proximity to the manufacturer, and differing degrees of quality standards are clear challenges. As a result, production schedule changes are becoming common because of poor supplier service levels, further affecting the ability of the supply chain to make and deliver on time.

Multiple manufacturing facilities. Large companies have anywhere from eight to 10 manufacturing plants with specialized capabilities at scattered locations. This has resulted in complex multilayer networks and material movement that not only affects inventory levels, but also increases overall supply chain costs.

Decentralized R&D centers. Companies use multiple in-house centers or third-party centers at different stages of drug development. This creates complexity in technology transfer, lengthening timelines for regulatory approval and impacting the first-to-file system. In addition, there is a risk of commercial batch failure, which increases costs and reduces plant utilization.

Complex and unequipped distribution network. Most third-party cold chain logistics providers do not have adequate capacity and temperature control systems to support today’s drug storage and handling requirements. In addition, pharma companies lose control over the supply chain beyond the distributor. Companies deal with thousands of distributors, which creates a lack of visibility and unreliable forecasting and results in suboptimal inventory and poor service levels.

Infrastructure gaps

India faces many gaps in its supply infrastructure, including in transportation, storage, and power supply. In transportation, less than 5 percent of roads are national highways, and they handle more than one-third of traffic. The rail network is similarly inadequate, and the air network in underutilized.3 In terms of storage, the lack of a robust cold chain network to support the supply chain represents a significant gap in today’s pharma infrastructure. Drugs have varying storage requirements to ensure that potency is maintained throughout their shelf life. Moving specialty products and vaccines requires continuous monitoring at all stages of the value chain, but with the current infrastructure, companies are still unable to ensure a product is stored at the required conditions throughout its transition.

Companies lose visibility and control of the product’s movement beyond the clearing and forwarding agents. In addition, many warehouses, distributors, and far-flung retailers do not have the infrastructure to store the product. The result is damaged products, rejects from customers, and greater risk to patients. To overcome external infrastructure constraints, the pressure for timely and effective supply chain execution becomes paramount.

The industry has much headway to make. The Indian cold chain market is highly fragmented with more than 3,500 companies. Organized players only contribute 8 to 10 percent of the cold chain industry market. Cold chain vendors are in dire need of both connectivity and technology. Vendor fleet trucks still use outdated equipment, which adds to the risk and uncertainty of delivering safe products to patients. As reported in Express Pharma, high operating costs— nearly double those in the United States—are one of the main reasons why truck fleet vendors are not investing in newer technology.

How to Gain a Competitive Edge

Several markets have seen steady growth over the past five to 10 years. China, Germany, Italy, and Brazil continue to be serious competition for India on both exports and imports. India lost to China when it was unable to cater to its own domestic demand for active pharmaceutical ingredients—75 percent of bulk drugs are still imported from China. Price increases driven by social and economic events, together with China’s increased focus on exports, pose a significant risk to raw material supply.

Now is the time to design a supply chain that is more adaptive, flexible, and responsive to changes in supply and demand. Otherwise, India could lose a large share of the global market, especially in high-margin businesses such as specialty and complex generics and biosimilars.

India’s pharma companies will need to change their supply chain game plan and focus efforts on four dimensions:

Reduce end-to-end complexity

Our study shows that managing complexity is on the top of industry leaders’ agendas. However, most companies have yet to launch structured efforts.

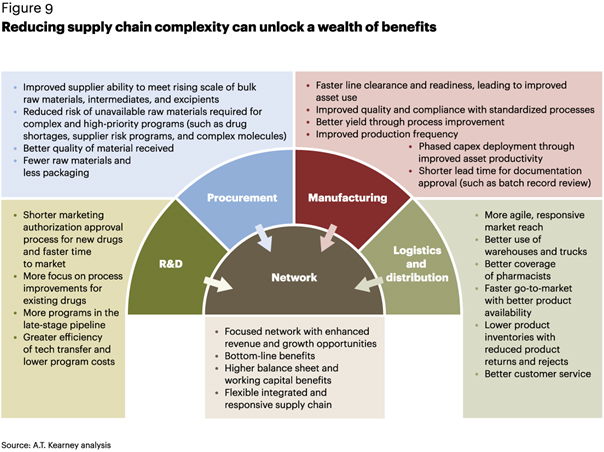

Reducing complexity can unleash an array of benefits (see figure 9). First, pharmaceutical companies must focus on consolidating and optimizing the network as a whole, also taking into account scenarios emerging from the possible GST regime. The supply chain operating model should support seamless communication across suppliers, manufacturers, distributors, and customers. Redundancies should be removed to improve supply chain efficiency and release “sunk” capacity. Consolidate capacities to align assets with capabilities and strategies, leading to top-line improvement. For example, Indian pharmaceutical company Cipla initiated a long-term capacity augmentation program that included supply-and-demand mapping and rationalization across all sites. As a result, it now has a good grip on complexity to help achieve its desired profitability and operational efficiency levels.

Second, companies need a tailored view of their supply chains. As they venture into more specialized products, segmentation based on consumers’ needs, product types, product attributes, and markets will be crucial to improving efficiency. Industry has still not effectively segmented the supply chain, which affects network performance and leads to reduced service levels, greater strain on production, and high supply chain costs. FMCG companies, however, have been quick to adopt segmentation and have captured significant value. For example, a large consumer high-tech electronics manufacturer in Asia with global operations was aligned geographically to its regional markets. Once the differences in consumer expectations and supply chain maturity became evident, the firm adopted two parallel supply chain segments. An efficiency-oriented build-to-stock model and service-level-oriented build-to-demand model were used to create premium segments. After segmentation, year-on-year growth increased by about 14 percent (three-year CAGR).

Finally, the portfolio’s complexity should be handled both upstream (R&D portfolio proliferation) and downstream (product SKU proliferation). There is an increasing trend to allocate more funds to R&D. Leading companies are continuously rationalizing their R&D portfolio to align with the overall commercial strategy and streamline their R&D pipeline. Looking downstream at commercial SKUs, individual pharma sites manufacture 1,000 to 3,000 SKUs per month, catering to multiple geographies. This can be reduced by optimizing capacity and resources upstream and by killing underperforming product lines and SKUs. As a result, companies can expect an immediate impact on overall flexibility of downstream processes with a significant reduction in supply chain costs.

Create agility and visibility in the supply chain

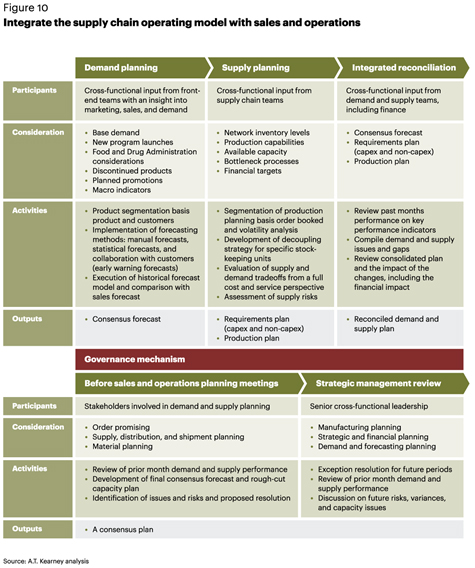

In addition to market dynamics such as changing patient needs and shifting disease patterns, the global market is experiencing significant drug shortages and more frequent outbreaks of communicable diseases. To react to these market changes and achieve best-in-class performance levels, companies need a supply chain operating model that is integrated with their S&OP processes and their commercial strategies (see figure 10).

Forward-thinking firms are moving from a “planning for convenience” model to a “planning for market” model. A.T. Kearney’s work with pharma and FMCG companies shows that planning functions need to be tightened with clear long-term, medium-term, and short-term plans across plants, products, and markets. Another important element is to have a clear inventory strategy, including replenishment norms that are defined across all nodes of the supply chain network. A.T. Kearney has helped companies tighten their processes across the value chain—resulting in an immediate increase in agility and greater flexibility in production.

According to our study, a few large players have initiated focused efforts to streamline their processes across the value chain. To operationalize this, there is a need for greater alignment across the value chain through strong cross-functional processes, which encourage a more effective flow of information and collaborative data-based decision making. End-to-end S&OP processes need to be more inclusive with clear accountability across internal and third-party stakeholders. This will result in greater transparency of supply-and-demand scenarios, stable production and inventory levels, and an ability to identify risks such as stock-outs or sudden demand spikes. Based on A.T. Kearney’s experience, companies see a 10 to 20 percent increase in service levels (from the current average of about 60 percent) by streamlining their S&OP processes, which typically leads to a 1 to 2 percent topline increase.

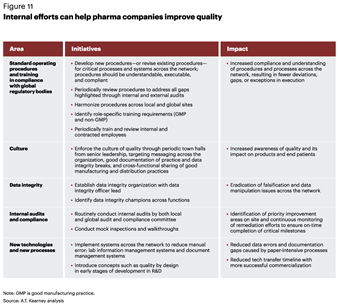

Build a robust quality and compliance system

There is an immediate need to tighten quality processes. The industry as a whole should move away from viewing quality as a support function and toward seeing it as a vital internal governance body. It is imperative to have a strong quality organization with visibility and oversight across all good manufacturing practices in the supply chain, both internal and external. Designing and implementing quality systems is about much more than having best-in-class procedures and systems. Leading companies know that quality is a strategic initiative that supports growth.

Indian pharma companies need to tighten their quality systems to be able to meet growing regulatory requirements and scrutiny. However, a few leading companies have taken structured initiatives to boost their quality standards and have received positive affirmation from global regulatory bodies such as the FDA. Based on our study, five internal initiatives can have a sizable impact on quality systems, resulting in overall efficiency and productivity in the supply chain (see figure 11).

In addition to internal quality issues, the executives we surveyed admit that a lack of transparency in the value chain poses a serious threat to quality compliance. Internal initiatives are an essential way to improve supplier quality, and companies are working closely with their third-party players to better control quality of materials and service. The quality system should include suppliers, contract manufacturers, and logistics providers. Large companies have begun to work with their suppliers to improve quality, but more focused efforts are needed to improve the quality of the network as a whole.

Use technology across the supply chain

Technology remains one of the most important areas for pharma companies to focus on. Leaders admit that one immediate result is greater transparency, which leads to better decision making. Technology can be used to integrate functions across the network, increase visibility of products across the value chain, and automate processes to improve the supply chain’s responsiveness and reliability.

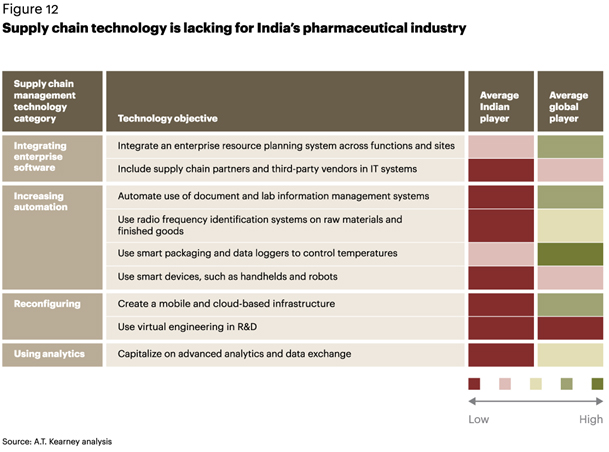

Our study reveals sizable gaps in the maturity of supply chain technology between a typical mid- sized Indian pharma company and a global firm (see figure 12). India continues to be slow to adopt newer technologies. Based on our study, companies should focus on four areas in the near term:

Integrating enterprise software. Although most pharma companies have an enterprise resource planning (ERP) system, it is often used for specific operations and not integrated with the larger network. For example, if a company is using ERP software to manage inventory, the location of raw materials and finished products is available only at a plant level and not at a cross-site level. Companies can achieve significant operational efficiency with more effective implementation and use of ERP systems.

Increasing automation. Large pharma companies are focusing on automation across the value chain. However, most have allocated very little capex to automation. Companies with effective automation have streamlined the work flows with fewer handovers and end-to-end transparency on costs and business value.

Improving tracking and visibility across the value chain. With rapid growth in the industry, pharma companies must use tracking technologies to streamline distribution and reduce lost revenue as a result of damaged products and recalls. Greater visibility during planning also optimizes inventory levels across all nodes.

What to Expect from Government and Industry Bodies

Supply chain improvements cannot be made in isolation but must occur across the ecosystem. However, some important initiatives are beyond the control of pharmaceutical firms. Strong interaction with government and industry bodies will be essential to making this happen.

Better enforcement of regulatory standards

Government has updated the Indian Pharmacopoeia Commission to improve quality standards, but responsibility does not stop there. For example, policies governing testing and release need to be reexamined to reduce risks to patients. Regulatory improvements are a good sign, but stricter governance and vigilance to enforce the standards are clearly needed. A number of collaborative industry-company consortiums are pushing for improvements, but most lack a robust task force to monitor implementation. Enforcement can be achieved by deploying high-potential task forces armed with a two-prong mission to build awareness and monitor industrywide execution. First and foremost, awareness needs to be built across the industry regarding regulations through funded training programs on core topics, pharma quality summits, best practices sharing groups, and FDA readiness workshops. It is also important to monitor change and review progress in close collaboration with company leaders.

Improvements in the overall pharma ecosystem

The government is allocating more of its budget to policies and programs to improve the overall pharma ecosystem. However, budget alone cannot ensure the success of these policies and programs. The immediate need is for collaboration between all key bodies to address a high- priority agenda with the following elements:

Support an increase in the production of active pharmaceutical ingredients by local players through capacity-building initiatives, manufacturing plant upgrades, and technology adoption, aided by collaborative development programs.

Focus efforts to reduce attrition across core areas (R&D, quality, and regulatory) to increase overall industry capabilities. (Currently attrition is 20–30 percent in the Indian pharma industry compared to 10–12 percent globally, according to analyst reports.) Increase focus on training through high-impact programs in partnership with educational institutions and development firms to enable employees to meet global standards.

Set up center-of-excellence units with participation from key personnel across Indian pharma companies to discuss learnings, best practices, and road map to upgrade quality standards.

Partner with cold chain players to define distribution network requirements. Capacity needs to seamlessly cater to local and global demand.

Support radio-frequency identification programs countrywide to decrease product losses.

Develop clusters of active pharmaceutical ingredients, and establish pharma parks to organize the sector, improve access to resources, and streamline production.

Infrastructure improvements

Infrastructure coupled with increased regulatory norms create additional hurdles for the Indian pharmaceutical industry. The 12th Five-Year Plan envisions more budgetary allocations in the logistics sector. Three initiatives will support the pharma ecosystem:

- Exemption from customs duty for refrigeration motor vehicles and allowance of 100 percent foreign direct investment (FDI) in storage and warehousing

- Augmentation of port-handling capacity to 3,200 metric tons by 2020 and allowance of 100 percent FDI in construction and maintenance of ports and harbors

- Development of additional expressways and national highways, as well as commissioning of dedicated freight corridors to increase rail freight

- Although these areas should be in focus to operationalize growth, addressing them will require cross-functional integration, structured planning, and commitment across the industry.

Revamping the Pharma Supply Chain

To realize their full supply chain potential, India’s pharma companies will need to revamp their models and processes. A supply chain transformation will be essential. This comprehensive change will require commitment from top management, coupled with a capable execution team that can help sustain the benefits. Although this is no small task, consumer goods companies that have built world-class high-performing supply chains have emerged as market leaders. Now is the time for pharma companies to follow suit and prepare for the future. Those that lead the way will capture a competitive advantage.

A Blockchain prescription for the Indian Pharmaceutical Industry

A major challenge facing the pharmaceutical industry today is the traceability and security of its supply chain, from raw material to manufacturing and on to the consumer. Blockchain may be the prescription to these problems.

A major challenge facing the pharmaceutical industry today is the traceability and security of its supply chain, from raw material to manufacturing and on to the consumer.

From tracing the quality of raw materials at source to maintaining the cold chain integrity of finished products in transit and managing drug recalls and safety announcements – these are just some of the industry’s supply-chain concerns.

Then there is the multi-billion-dollar global industry of counterfeit medicines. A 2014 Associated Chambers of Commerce of India (ASSOCHAM) report put the percentage of counterfeit drugs in India alone at a staggering 25 percent. Not only is this an issue for the industry but also for unsuspecting patients.

The industry has developed tracking solutions with barcodes or radio-frequency identification (RFID) tags, but the syncing of data across the different suppliers is inefficient. Data is not available in real-time and the systems are susceptible to fraud and manipulation.

Enter Blockchain

Blockchain may be the prescription to these problems. This distributed, decentralized ledger is managed collectively by a set of stakeholders who basically don’t trust each other. Each entry in the ledger is cryptographically secured, and made immutable by linking it to the previous entry using cryptographic hashes. Each major stakeholder runs a blockchain node that instantly mirrors the transactions taking place in the network, keeping the ledger in sync.

The pharmaceutical supply chain blockchain could be a ‘private’ blockchain, overseen by a government regulator. The parties involved in the supply-chain log their data into a common blockchain. The production factory logs the production date and time of each batch and unit. The loading dock logs when a batch was loaded onto the truck. The temperature sensors on the truck report real-time temperatures into the blockchain, and so on.

This level of real-time visibility to all stakeholders means problems can be detected and remediated quickly. The data is also immune from tampering. When a consumer buys a medicine, they can also scan the barcode on the packet to instantly verify the authenticity of the medicine from the blockchain and receive any alerts about it.

Blockchain and Regulatory Compliance

In India, the Directorate General of Foreign Trade (DGFT) has mandated serialized tracking of exported pharmaceutical products down to the strip or vial, as well as sharing and archiving this data. The US FDA’s Drug Quality and Security Act (DQSA) specifically has compliance mandates for supply chain security.

A blockchain-enabled trace and track system makes it easier for manufacturers to comply with such regulations globally and provide regulators with a high-integrity audit trail visible in real-time.

Beyond supply-chain, blockchain can also positively impact clinical trials. According to the World Health Organization (WHO), 50% of clinical trials don’t report a result and industry-sponsored trials are four times more likely to declare positive results than others. Trials can suffer from incorrect consent reporting, data fudging or selective inclusion.

Blockchain offers a superior way to ensure accuracy and integrity of the outcome. An immutable blockchain would mitigate data fudging, selective reporting and any risk of consent fraud. In a recent survey of 120 pharmaceutical and life science executives by the Pistoia Alliance, 83% expected to adopt blockchain within five years and 68% expected blockchain to have the biggest impact in securing the supply chain.

Regulatory issues and data privacy were perceived as the two top hurdles to adoption. These are short-term hurdles. Globally, regulators are reviewing how blockchain can help the industry and the blockchain community is adding data privacy to the platforms.

To the leaders in the pharmaceutical industry, I recommend starting with a proof-of-value prototype, followed by a pilot with a limited set of partners. This will set you on the right path to adoption with minimal risk but optimal outcomes.